Imagine finding a financial tool so reliable that it shields your wealth from market volatility, guarantees compounding growth, and offers complete tax immunity. For decades, traditional savings accounts have failed to outpace inflation, leaving everyday investors scrambling for safety.

Enter the Public Provident Fund (PPF).

When you open a PPF account at a Post office, you are tapping into one of India’s most trusted and time-tested wealth-creation vehicles. Backed by a sovereign guarantee, it ensures your hard-earned money is completely secure. But here is the catch: simply opening an account is not enough.

To truly build a multi-lakh or even multi-crore corpus, you need to understand the math behind the magic. This is where a PPF calculator becomes your best financial friend. By mapping out your investments year by year, you remove the guesswork from your retirement or long-term financial planning.

In this comprehensive guide, we will break down exactly how to leverage a PPF calculator to project your earnings, compare the PPF against other popular investment options, and reveal insider strategies to legally maximize every single rupee of your tax-free returns.

What Makes the Post Office PPF So Powerful in 2026?

Before diving into the numbers, it is vital to understand the foundational rules of the scheme for the 2026 financial year. The government has maintained the interest rate at an attractive 7.1% per annum, compounded annually.

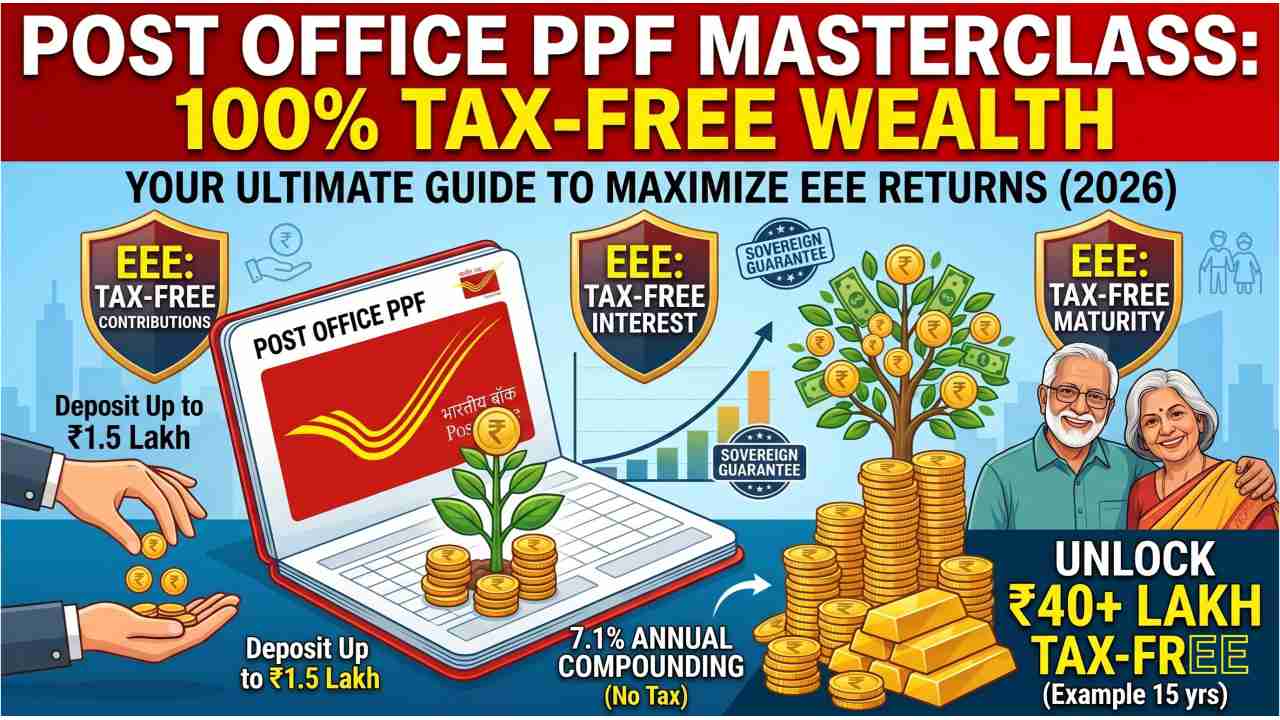

Unlike stock market investments, which can swing wildly based on global economic factors, your PPF balance moves in only one direction: up. It offers the coveted “EEE” (Exempt-Exempt-Exempt) tax status. This means your yearly contributions (up to ₹1.5 lakh) are tax-deductible under Section 80C of the old tax regime.

Furthermore, the interest you earn every year is completely tax-free. Finally, when you withdraw your maturity amount after the 15-year lock-in period, that entire lump sum is also entirely exempt from income tax.

From the busy streets of Mumbai to a peaceful local branch in Kokrajhar, the sovereign guarantee and the 7.1% interest rate remain absolutely identical. The playing field is entirely level, rewarding only one thing: disciplined, long-term consistency.

Demystifying the PPF Calculator: How It Actually Works

At its core, a PPF calculator is an algorithmic tool designed to project the future value of your investments over the mandatory 15-year tenure. It requires three primary inputs from the user: your yearly deposit amount, the current interest rate, and the total tenure.

Let’s look at how the calculation functions behind the scenes.

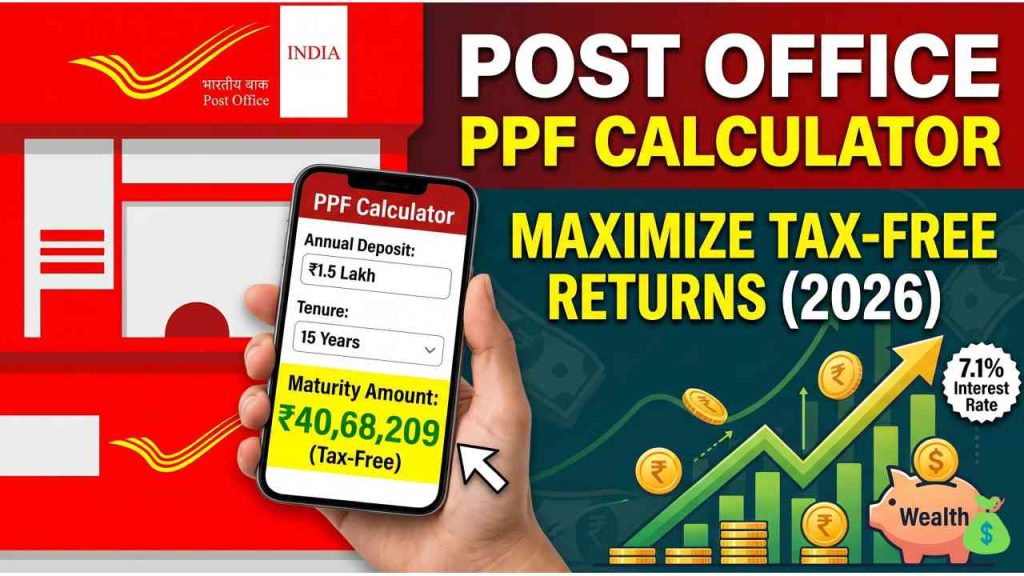

If you deposit the maximum allowable limit of ₹1,50,000 every year for 15 years, your total out-of-pocket investment will be ₹22,50,000. Assuming the interest rate remains constant at 7.1%, the calculator uses the formula for compound interest to determine your yearly accrual.

By the end of the 15th year, your total interest earned will be roughly ₹18,18,209. When added to your principal, your maturity amount balloons to a staggering ₹40,68,209.

Using an online calculator allows you to experiment with different contribution amounts. If you can only afford ₹50,000 a year, the tool instantly recalibrates to show a maturity value of approximately ₹13,56,070. This immediate visual feedback is essential for setting realistic, achievable financial goals without relying on complicated manual spreadsheet formulas.

The “5th of the Month” Rule: A Crucial Insight

If there is one section of this guide you memorize, let it be this one. The way interest is calculated on a PPF account is highly specific, and ignoring it can cost you thousands of rupees over your investment tenure.

While the interest is compounded annually and credited to your account on March 31st every year, it is actually calculated on a monthly basis.

The post office calculates your monthly interest based on the lowest balance in your account between the close of the 5th day and the last day of the month. If you deposit your monthly contribution on the 6th of the month, that money will not earn any interest for that entire month.

To maximize your returns, you must ensure your deposits are credited on or before the 5th of the month. If you are making a lump sum deposit for the entire year, doing so before April 5th will guarantee you earn interest on that full amount for all 12 months of the financial year.

Comparison: Post Office PPF vs. Other Savings Options

It is natural to wonder if tying up your money for 15 years is the best move. Much like our recent deep dive into the Post Office Fixed Deposit calculator, understanding how to project your returns requires comparing apples to apples across the financial landscape.

Let us evaluate how the PPF stacks up against other popular instruments in 2026.

PPF vs. Fixed Deposits (FDs)

Fixed deposits offer high security and predictable returns. Currently, many banks and post offices offer FD rates hovering around 7.0% to 7.4% for specific tenures. However, FDs strictly lack the EEE tax benefit. for more visit official post office website.

The interest you earn on a standard FD is added to your taxable income and taxed according to your income slab. If you are in the 30% tax bracket, a 7.1% FD yields a net return of less than 5%. In contrast, the PPF’s 7.1% is a net, tax-free return, making it vastly superior for high-income earners.

PPF vs. Equity Linked Savings Scheme (ELSS)

ELSS mutual funds also offer Section 80C tax benefits and have a much shorter lock-in period of just three years. Historically, equity markets can deliver double-digit returns (10% to 15%) over the long term, easily outpacing the PPF.

However, ELSS funds are subject to market volatility. Your principal is not guaranteed, and returns are subject to Long-Term Capital Gains (LTCG) tax of 12.5% above ₹1.25 Lakh. The PPF is for your debt portfolio—the bedrock of your financial security—while ELSS should be used for aggressive wealth expansion.

PPF vs. National Pension System (NPS)

While the NPS allows for higher equity exposure and an additional ₹50,000 tax deduction under Section 80CCD(1B), it comes with rigid withdrawal rules. It mandates that 40% of your maturity corpus must be used to purchase an annuity (a regular pension), which is fully taxable as income. The PPF gives you 100% tax-free liquidity at maturity, offering unparalleled freedom on how you spend your retirement corpus.

📊 Investment Comparison: Navigating Your Options

| Feature | Post Office PPF | Bank Fixed Deposit (FD) | ELSS Mutual Funds |

| Lock-in Period | 15 Years | 1 to 5 Years | 3 Years |

| Current Return | 7.1% (Variable quarterly) | ~6.5% – 7.4% (Fixed) | Market Linked |

| Risk Level | Zero (Sovereign Guarantee) | Very Low | High (Equity Risk) |

| Tax on Interest | Completely Tax-Free | Taxable per income slab | 12.5% LTCG |

| Best Suited For | Retirement, safe long-term wealth | Short-term secure goals | Aggressive growth |

(Note: Data reflects general market conditions as of Q2 2026).

Key Insights: Strategies to Maximize Your PPF Returns

Simply opening a PPF account is a great first step, but optimizing it requires strategy. Here are advanced insights to ensure you are squeezing every ounce of value from your investment.

1. Front-Load Your Investments

As mentioned earlier, if you have the liquidity, deposit your entire ₹1.5 lakh limit before April 5th of the new financial year. By doing this, you earn the 7.1% interest on the full amount for the entire 12-month cycle.

Consider the math: ₹1.5 lakh invested annually on April 1st yields ₹40.68 lakh at maturity. However, investing ₹12,500 monthly on the 10th of every month yields roughly ₹39.44 lakh. That is a difference of over ₹1.2 lakh lost simply due to the timing of your deposits!

2. Extend Beyond 15 Years

The 15-year maturity mark is not a hard stop; it is a massive opportunity. Once your account matures, you have the option to extend it in blocks of 5 years, indefinitely. You can choose to extend it with fresh contributions or without fresh contributions.

If you extend with contributions, you continue to get 80C benefits while your massive accumulated corpus continues to compound. Because the principal is already so large after 15 years, the interest earned during these 5-year extension blocks is staggering. The compounding curve turns truly vertical during these extension phases.

3. Strategic Partial Withdrawals & Loans

Liquidity is often cited as the PPF’s biggest drawback, but it is not entirely rigid. The scheme allows for partial withdrawals from the 7th financial year onward. Furthermore, you can avail of a loan against your PPF balance between the 3rd and 6th financial year at a nominal interest rate (1% above the PPF rate).

While it is always best to leave compounding uninterrupted, knowing these lifelines exist makes it easier to commit larger sums to the account without fearing total illiquidity in a family emergency.

The Psychological Benefit of the Lock-In Period

While many financial gurus criticize the 15-year lock-in, seasoned investors know it is actually a hidden superpower. Human behavior is arguably the biggest threat to wealth creation. We panic during market crashes, and we get greedy during bull runs, often pulling money out prematurely to fund lifestyle upgrades.

The strict lock-in rules of the Post office PPF act as a behavioral guardrail. It forces financial discipline. It ensures that the money you earmark for your older self actually survives long enough to reach them. You cannot impulsively liquidate a PPF to buy a new car or upgrade your smartphone.

For gig-economy workers, freelancers, and entrepreneurs who experience fluctuating monthly incomes, the flexibility to deposit as little as ₹500 in lean months and up to ₹1.5 lakh in profitable months makes it an incredibly forgiving framework. It transforms casual savers into generational wealth builders.

Step-by-Step: Opening and Managing Your Post Office PPF

Gone are the days of standing in endless queues with physical passbooks. Today, opening and managing your Post office PPF is highly streamlined.

- Gather Your Documents: You will need your Aadhaar card, PAN card, passport-size photographs, and the account opening form (Form-1) available at the post office or online.

- Initial Deposit: You can start with as little as ₹500. Ensure you maintain this minimum deposit every financial year to prevent your account from becoming inactive (which incurs a ₹50 penalty to revive).

- Automate Deposits: Set up a standing instruction or automated bank mandate to transfer your chosen amount before the 5th of every month.

- Track Annually: Use an online PPF calculator once a year to track your actual growth against your projected goals. Adjust your yearly contributions if your income increases.

- Update Nominees: Always ensure your nomination details are up to date and your KYC is fully compliant with the latest 2026 regulations to avoid sudden account freezing.

Conclusion

Navigating the landscape of personal finance does not have to be an exercise in high-risk speculation. The humble Post office PPF remains an undisputed heavyweight champion of risk-free, tax-efficient wealth generation.

By utilizing a PPF calculator, adhering strictly to the 5th of the month rule, and understanding the sheer power of 5-year extensions, you can transform a simple savings habit into a robust retirement fund. It requires patience, yes, but the math is undeniable. The compounding engine is real, and the tax benefits remain unmatched in the current financial ecosystem.

It is time to stop guessing and start projecting. Take control of your financial destiny today.

Are you ready to see how much your savings could grow? Use a PPF calculator today to run your own numbers! Drop a comment below with your target retirement age, or share this guide with a friend who is just starting their investment journey. Let’s build a wealthier, more financially literate future together.